Compare, Choose, Save.

Discover financial options with LoanZoom, the online comparison site. See different loans, make smart choices, and save money your way.

Get speedy and straightforward online loans in South Africa

Get the money you need from trustworthy lenders. Use one easy online form to apply for different types and amounts of loans.

Now, compare lenders and their loan options easily to find the best rates and repayment plans for you!

There are lots of loan offers available, so you can find one that meets all your needs easily.

Explore Loan Options and Compare Rates

📌 Frequently Asked Questions

🤔 What types of loans can I find on LoanZoom?

📝 At LoanZoom, our comprehensive array of financial solutions extends beyond personal loans and home loans to include additional options tailored to diverse needs. Whether you’re navigating short-term financial challenges, looking for quick access to funds with payday loans, or seeking a comparison of credit cards, we’ve got you covered.

📝 Our short-term loans are designed to provide quick and convenient financial assistance for immediate needs. Additionally, we offer payday loans for those seeking short-term borrowing solutions tied to their upcoming paycheck. If you’re exploring credit card options, our platform provides a comparison tool to help you make an informed decision based on your preferences and financial goals.

📝 Understanding that credit history can pose challenges, we also offer bad credit loans to provide accessible options for individuals with less-than-perfect credit scores. At LoanZoom, inclusivity is a priority, and our bad credit loan offerings aim to support those facing credit challenges.

📝 Our commitment is to empower you with a diverse range of financial tools and lending options. Whether you’re navigating everyday expenses, homeownership aspirations, short-term financial needs, or credit challenges, LoanZoom strives to be your partner in achieving financial success. Explore our offerings, compare options, and find the financial solution that best suits your unique circumstances.

🤔 What is a personal loan?

📝 A personal loan is when you borrow money from a bank or a lending company for your personal needs. It could be for things like paying off bills, taking a vacation, or handling unexpected expenses.

📝 With a personal loan, you agree to pay back the borrowed amount in monthly installments over a set period. The lender may charge you interest, which is an extra amount you pay for borrowing the money.

📝 Personal loans are unsecured, meaning you don’t need to provide collateral (like your car or house). They offer flexibility for various purposes, but it’s important to manage repayments responsibly.

🙋♂️ Lenders for Personal Loans

-

Capfin Loans

- Loans up to R50,000

- Term up to 12 months

- Interest up to 29.25%

-

Absa

- Loans up to R350,000

- Term up to 84 months

- Interest up to 13,75%

-

Finchoice

- Loans up to R40,000

- Term up to 24 months

- Interest up to 24%

-

Boodle Loans

- Loans up to R8,000

- Term up to 6 months

- Interest up to 60%

🤔 What is a short-term loan?

📝 A short-term loan is when you borrow a small amount of money for a brief period. It’s like a quick solution for when you need extra cash to cover something urgent, like unexpected bills.

📝 You agree to pay back the borrowed money within a short time, usually a few weeks or months. These loans are not for big things like buying a house but can help with immediate needs. It’s important to understand the terms and make sure you can repay the loan on time because short-term loans often have higher interest rates.

🙋♂️ Lenders for Short-term Loans

-

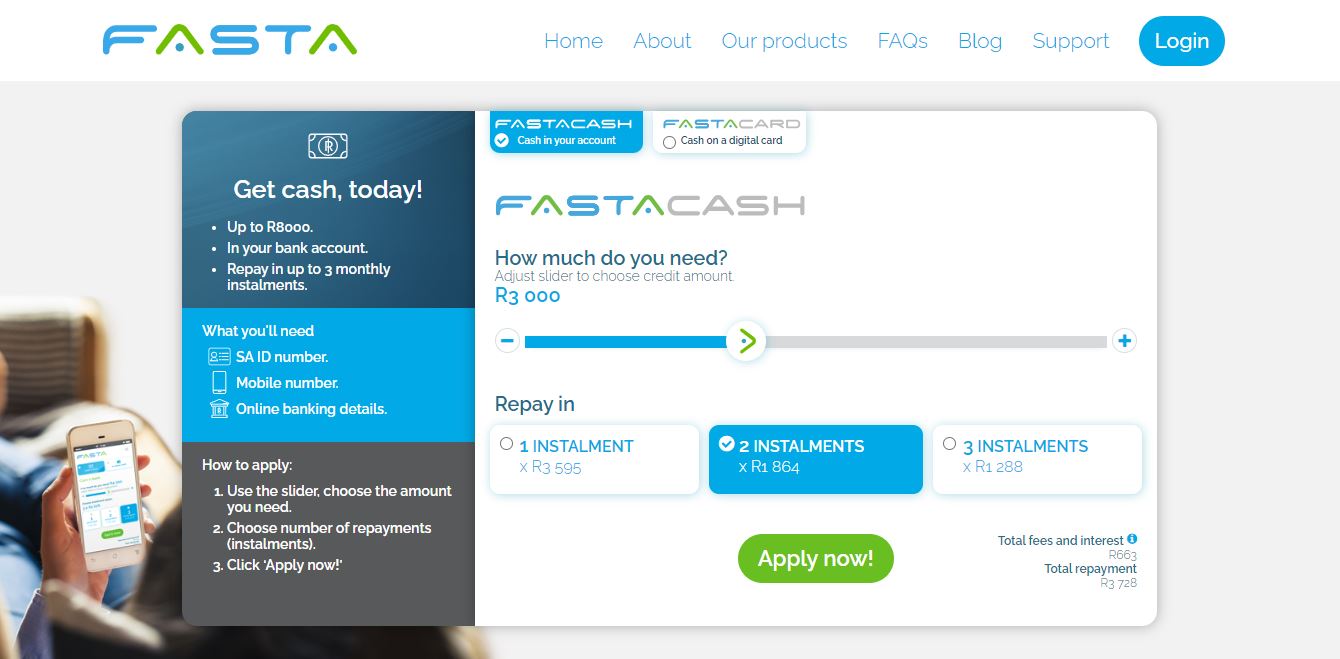

Fasta Loans

- Loans up to R8,000

- Term up to 3 months

- Approval in minutes

-

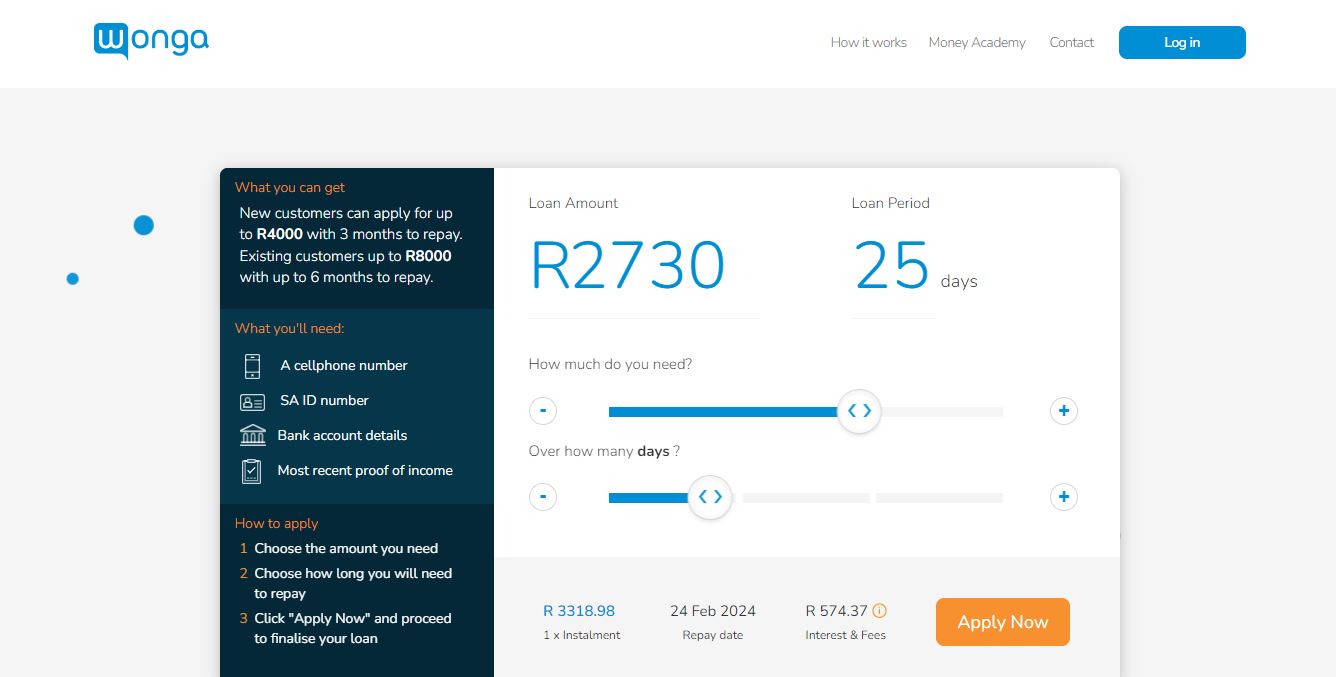

Wonga

- Loans up to 8,000

- Term up to 12 months

- Flexible interest rates

-

Finchoice

- Loans up to R40,000

- Term up to 24 months

- Interest up to 24%

-

Boodle Loans

- Loans up to R8,000

- Term up to 6 months

- Interest up to 60%

Online Loan Calculator

🤔 Can I get a loan with bad credit or being blacklisted?

📝 Wondering about loans with bad credit or being blacklisted? You may still have options. Despite a challenging credit history, some lenders specialize in assisting individuals in similar situations.

📝 While traditional loans might be tougher to secure, there are alternatives available. Explore tailored solutions designed for those with less-than-perfect credit.

📝 Keep in mind that interest rates may vary, so it’s crucial to carefully compare and choose the option that suits your needs.

📝 Seeking advice from financial experts or using specialized platforms can help navigate this process, increasing your chances of finding a suitable loan despite credit challenges.

🙋♂️ Lenders for Bad Credit Loans

-

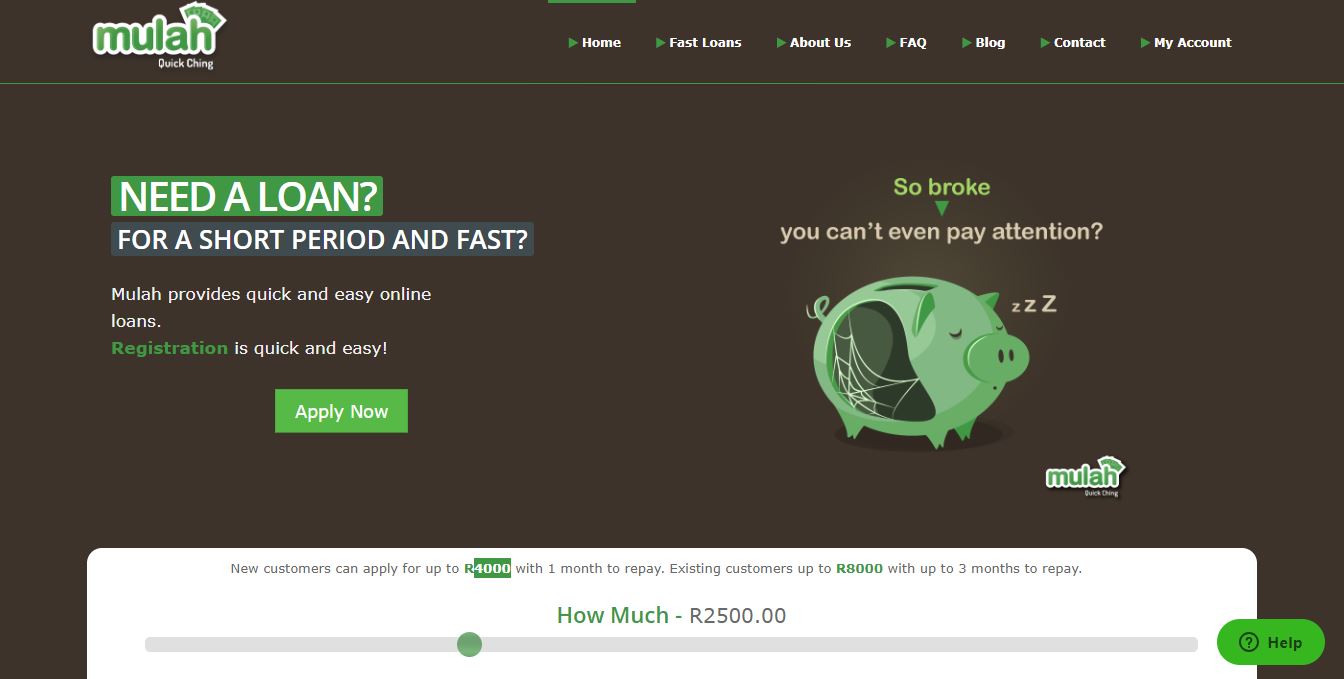

Mulah Loans

- Loans up to R8,000

- Term up to 3 months

- Interest up to 38%

-

Hoopla Loans

- Loans up to R250,000

- Term up to 60 months

- Interest up to 20%

-

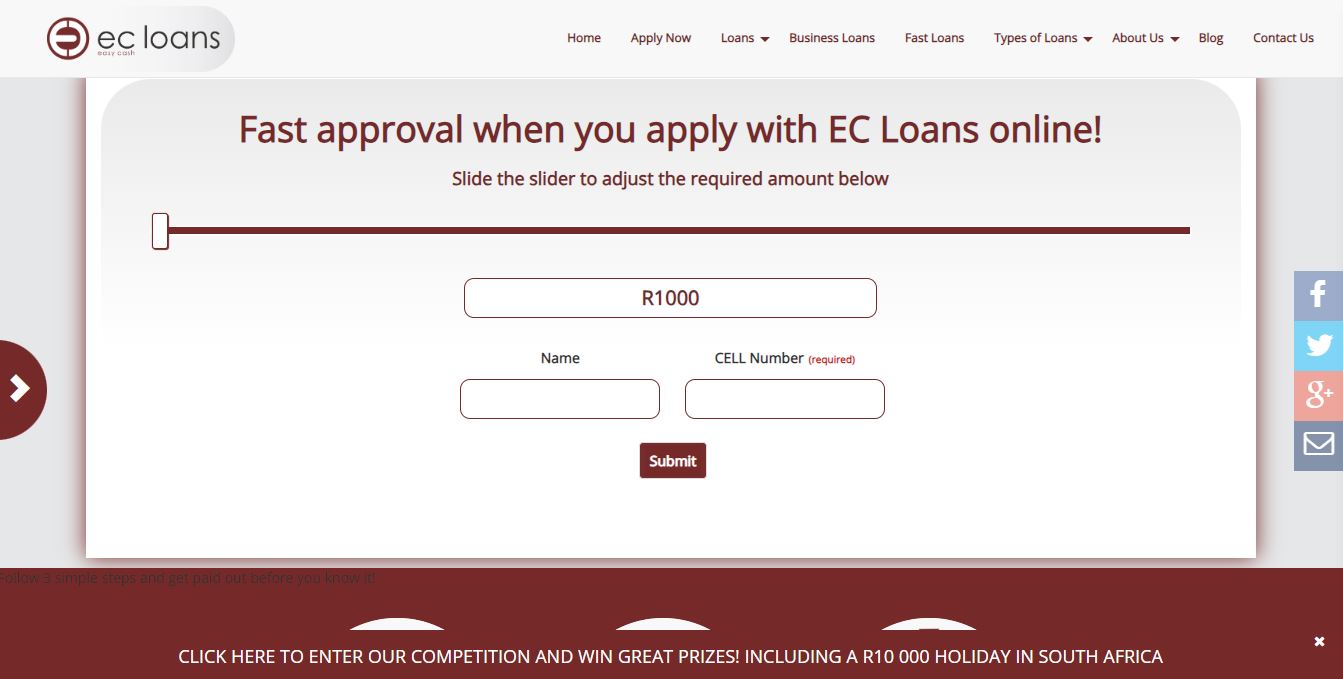

EC Loans

- Loans up to R120,000

- Term up to 84 months

- Interest up to 28%

-

EZI Finance

- Loans up to R8,000

- Term up to 6 months

- Interest up to 32.1%

🤔 What is a payday loan?

📝 Payday loans are a type of short-term borrowing where you can get a small amount of money quickly, usually to cover unexpected expenses or bills. Payday loans from LoanZoom are designed to be repaid on your next payday. They’re easy to apply for, often online, and approval is typically based on your income and employment.

🤔 How do you qualify for payday loans?

📝 To qualify for payday loans, you usually need to have a job or a regular source of income. The lender wants to make sure you can repay the loan when you get your next paycheck. You’ll also need a bank account, as they often deposit the loan money directly into your account and withdraw the repayment on your payday.

📝 Some lenders may check your credit, but many payday lenders are more concerned about your income and ability to pay back the loan. Keep in mind that each lender may have slightly different requirements, so it’s important to check with them directly.

🙋♂️ Lenders for Payday Loans

-

Fasta Loans

- Loans up to R8,000

- Term up to 32 days

- Approval in minutes

-

Wonga

- Loans up to 8,000

- Term up to 12 months

- Flexible interest rates

-

Lime24

- Loans up to R8,000

- Term up to 37 days

- Interest up to 24%

-

Boodle Loans

- Loans up to R8,000

- Term up to 32 days

- Interest up to 60%

🤔 What is a home loan?

📝 A home loan, commonly referred to as a mortgage, is a financial arrangement wherein an individual borrows money from a lending institution, usually a bank or a mortgage lender, to facilitate the purchase of a residential property, such as a house or an apartment. This borrowing serves as a crucial means for individuals who may not have the immediate funds to buy a home outright.

📝 The borrower, also known as the homebuyer, agrees to repay the borrowed amount in regular monthly installments over an extended period, which can span several years. These installments consist of both the principal amount borrowed and the interest charged by the lender. The principal is the original loan amount, while the interest is the cost of borrowing, calculated as a percentage of the outstanding loan balance.

📝 The extended repayment period, often ranging from 15 to 30 years, allows borrowers to manage the financial commitment more comfortably. It also enables individuals to make homeownership more accessible by spreading the cost over an extended timeframe.

📝 The home serves as collateral for the loan, meaning that if the borrower fails to make the required payments, the lender may have the right to take possession of the property through a legal process known as foreclosure.

📝 Overall, home loans play a pivotal role in helping people achieve the significant milestone of homeownership by providing a structured and affordable way to fund the purchase of a home. The terms and conditions of home loans can vary, and individuals are advised to carefully review and understand the terms before committing to such a substantial financial undertaking.

🤔 How do I qualify for a home loan?

📝 Qualifying for a home loan involves a thorough evaluation of various financial and personal factors by the lender. Here’s a breakdown of the key elements that lenders typically consider:

1️⃣ Credit Score

📝 Your credit score is a numerical representation of your creditworthiness, based on your credit history. Lenders use this score to assess the risk of lending to you. A higher credit score generally indicates a more reliable borrower. Individuals with higher credit scores often qualify for better interest rates and loan terms.

2️⃣ Income

📝 Lenders assess your income to ensure that you have a reliable source of funds to make monthly mortgage payments. A stable and verifiable income is crucial for loan approval. Lenders may consider your gross income, which is your earnings before deductions, to determine your repayment capacity.

3️⃣ Employment History

📝 A consistent and steady employment history is generally favorable when applying for a home loan. Lenders may verify your employment to assess the stability of your income. However, different lenders may have varying requirements regarding employment history, and self-employed individuals may need to provide additional documentation.

4️⃣ Debt-to-Income Ratio (DTI)

📝 Your debt-to-income ratio is a comparison of your monthly debt payments to your gross income. Lenders use this ratio to evaluate your ability to manage additional debt, such as a mortgage. A lower DTI ratio is generally favorable, indicating that you have more income available to meet your financial obligations.

📝 Lenders combine these factors to gauge the overall risk associated with lending to you. While specific requirements can vary among lenders, they typically seek a balance between your ability to repay the loan and the potential risks involved.

📝 It’s important for prospective homebuyers to be proactive in managing their credit, maintaining a stable income, and minimizing existing debts to enhance their eligibility for a home loan. Additionally, understanding these key qualification factors can empower individuals to address potential concerns and take steps to improve their financial profile before applying for a mortgage.

🙋♂️ Lenders for Home Loans

-

SA Home Loans

- Loans up to R1,000,000

- Term up to 30 years

- Interest from 10%

-

Standard Bank

- Loans up to 5,000,000

- Term up to 30 years

- Interest up to 15%

-

FNB

- Loans up to R5,000,000

- Term up to 20 years

- Interest up to 15%

-

Absa

- Loans up to R5,000,000

- Term up to 30 years

- Interest up to 15%

🤔 What is vehicle finance?

📝 Vehicle finance in South Africa refers to a financial arrangement that enables individuals to purchase a vehicle without paying the entire amount upfront. In this process, individuals borrow money from a financial institution, like a bank or a credit provider, to cover the cost of the vehicle. The borrowed amount is then repaid over a specified period through regular installments, which include both the principal amount (the initial loan) and interest charged by the lender.

📝 Common types of vehicle finance in South Africa include auto loans and vehicle leases. With an auto loan, individuals borrow a specific amount to buy the vehicle, becoming the owner once the loan is fully repaid. Vehicle leases, on the other hand, allow individuals to use a vehicle for a set period by making monthly payments but typically do not confer ownership at the end of the lease term.

🤔 Can I finance a used vehicle?

📝 You can get a loan to buy either a new or a used car from different lenders. But, keep in mind that the interest rates (the extra money you pay for borrowing) and the terms (how long you have to repay) can be different depending on the lender. It’s important to check and compare to find the best deal for you.

🤔 What documents are required for vehicle finance?

📝 To get a vehicle loan, you usually need to show documents like your ID, proof of income, and information about the car you’re buying. These documents help the lender verify your identity, assess your ability to repay the loan, and confirm details about the vehicle.

🙋♂️ Lenders for Vehicle Finance

-

Absa Vehicle Finance

- Loans up to R5,000,000

- Term up to 72 months

- Interest from 18%

-

WesBank Vehicle Finance

- Loans up to 5,000,000

- Term up to 72 months

- Interest up to 15%

-

Standard Bank Vehicle Finance

- Loans up to R5,000,000

- Term up to 72 months

- Interest up to 15%

-

MFC Vehicle Finance

- Loans up to R5,000,000

- Term up to 72 months

- Interest up to 15%

🤔 What is a credit card?

📝 A credit card is a financial tool provided by banks or financial institutions, typically in the form of a small plastic card. It enables individuals to make purchases with borrowed money, essentially creating a short-term loan. Users are assigned a credit limit, which represents the maximum amount they can borrow using the card. This limit is determined based on factors such as credit history and financial standing.

📝 When making purchases with a credit card, users are expected to repay the borrowed amount. At the end of each billing cycle, a statement is provided detailing the purchases made and the total amount owed. Users have the option to either pay the full balance by the due date or pay a minimum amount.

📝 If the full balance is not paid by the due date, interest is charged on the remaining amount. The interest rate, known as the annual percentage rate (APR), is set by the credit card issuer. Responsible use of a credit card, including timely payments, can positively impact an individual’s credit score, making it a useful tool for building creditworthiness.

🙋♂️ Lenders for Credit Cards

-

FNB Credit Card

- Credit limit up to R500,000

- Benefits No charge for Global Travel Insurance

- Build a credit history

-

Absa Credit Card

- Credit limit up to R500,000

- Benefits No charge for Global Travel Insurance

- Build a credit history

-

Woolworths Credit Card

- Credit limit up to R500,000

- Benefits No charge for Global Travel Insurance

- Build a credit history

-

NedBank Credit Card

- Credit limit up to R500,000

- Benefits No charge for Global Travel Insurance

- Build a credit history